PhonlamaiPhoto

PhonlamaiPhoto

CRISPR seems to be the preferable Gene Editing Method and CRISPR Therapeutics AG (NASDAQ:CRSP) could be on the right side in one of the potential biggest disruptive technology in biotech. The company is investing $0.5B in a year and is focused on innovation and growth. The company has its production plant and seems flexible on market demand and commercial agreements. Founded in 2013, ten years later, the time seems to have come to see the first product (based on thalassemia and sickle cell disease) on the market. At the moment, the company balance sheet seems to be able to support company growth and shows competitive share price valuation parameters when compared to the median sector or CRISPR competitors.

The risks of an investment in CRSP are many and high, especially in terms of time horizon and volatility but the possible positive return could be very high. Some companies have reached the $100 billion goal with a single drug and the question may be: can CRSP emulate that result in the next 10 years? I don’t know if the goal will ever be achieved but the foundations for being able to do well are there right now and I think there can be good returns in the long run. My rating is Buy.

Current pharmaceutical drugs seem to have limited or no success with some rare and common diseases and gene-editing-based Companies set themselves the mission to treat genetic diseases by deleting, correcting, and inserting genes. CRISPR/Cas9 is a disruptive technology based on gene editing or technology for altering sequences of genomic DNA (Deoxyribonucleic Acid). CRISPR means Clustered Regularly Interspaced Short Palindromic Repeats. Cas9 is a specific protein 9.

Dr. Emmanuelle Charpentier (Director of the Max Planck Unit – Berlin, Germany) studied and analyzed how Cas9 can be used to cut, in certain locations, the double-stranded DNA. Dr. Charpentier and Dr. Doudna (Berkeley University – California) get the Nobel Prize in 2020 as a consequence of their studies on this technology.

CRISPR Therapeutics AG acquired the rights to the intellectual property for CRISPR/Cas9 and could be defined as a gene editing company based on CRISPR/Cas9 technology.

CRISPR Form 10-K

CRISPR Form 10-K

The main company products are based on CRISPR/Cas9 platform with an ‘ex-vivo’ strategy. Ex-vivo means that the studies (gene-edited cells) are conducted outside the human body before the administration to the patients. On one other side, the Company also develops in-vivo studies which mean that the therapy is directly administered within the patient body.

The two main programs are ex-vivo with TDT (transfusion-dependent-thalassemia) and SCD (sickle-cell-disease) and represent a big market opportunity because of two hemoglobinopathies with high medical market demand with low or no supply.

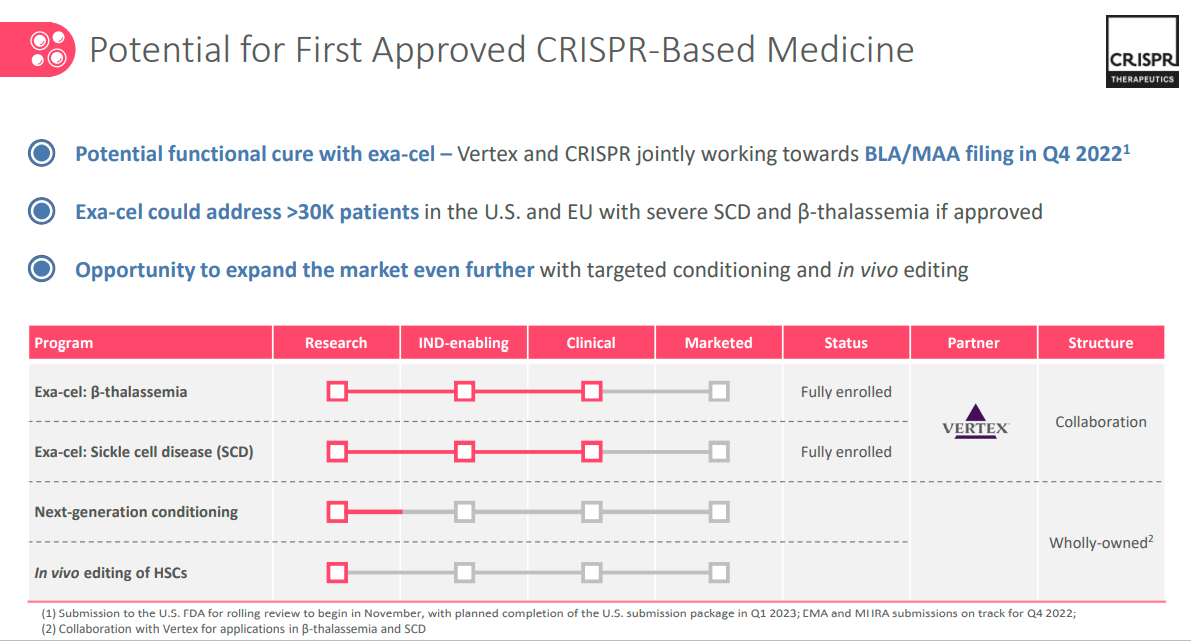

The main hemoglobinopathies product is CTX001 and is used in patients with TDT and SCD diseases. CRISPR Therapeutics in partnership with Vertex (VRTX) is developing CTX001 in a Phase-3 clinical trial both in Beta-Thalassemia (TDT) and Sickle Cell Disease (SCD) in patients between 12 to 35 years old. CTX001 has received several regulatory designations from the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) for both TDT and SCD treatment.

The company is developing also programs for the treatment of hematological and solid tumor cancers and type 1 diabetes (T1D). This is the immuno-oncology company’ area that studies and develops products based on T or CAR-T cell therapies. This is also an ex-vivo program and the main product is named CTX110. CTX110 is in Phase 1 clinical trial and is in a regenerative medicine advanced therapy (RMAT) designation by the FDA.

Regenerative Medicine represents another big company program. Regenerative medicine means the repair or replaces tissue or organ by the use of stem cells. This kind of therapy could be used for common or rare diseases.

Lastly, in-vivo programs should also be mentioned which aim to treat diseases related to the nervous system, muscles, liver, and lungs.

CRISPR Corporate Overview Q4 – 22

CRISPR Corporate Overview Q4 – 22

The CTX001 is in BLA (Biologics License Application) status which means that the Company is requesting to FDA the permission to introduce the product into commerce. The same status is in Europe with EMA.

One of the main concerns could be related to the FDA and EMA approach and it seems that the two government bodies appear aligned and, according to management, are offering a supportive approach for the formulation of the final BLA before commercialization.

Listening to the last CRISPR Therapeutics AG – Morgan Stanley 20th Annual Global Healthcare Conference:

‘We’ve recently said that we’ve completed sort of the pre-BLA meetings with the FDA. We’re ironing out a few of the last details and we’ll provide guidance in the next few weeks around when the exact BLA timing would be. But I think we’re — we’ve completed all the discussion on the European side, almost there with the FDA and I think we look forward to filing for regulatory approval across both side of the ocean soon.’

We can hypothesize that 2023 could be the year in which the CTX001 will be placed on the market.

CRISPR Corporate Overview Q4 – 22

CRISPR Corporate Overview Q4 – 22

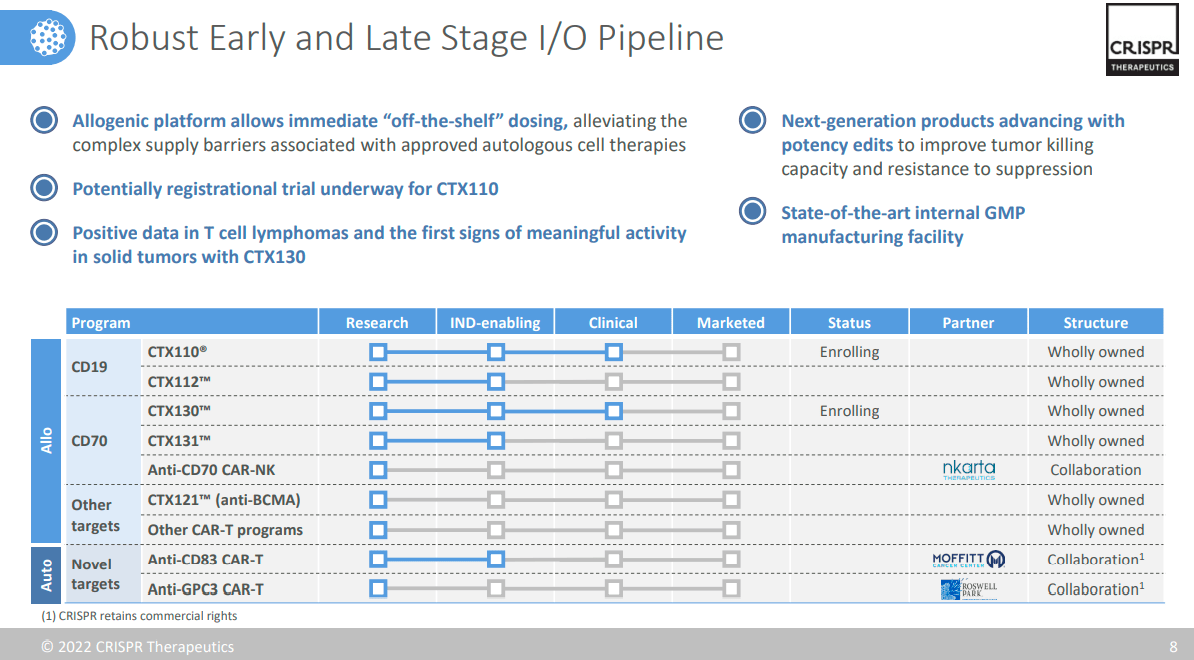

CTX110 is in an enrollment clinical status and it means that it could be the next product that will be able to begin the preliminary discussions with the regulatory bodies to move on to a final marketing request phase. It is expected it could be a $1 billion drug product with an open door for formal approval.

Related to the other allogenic programs the company is a pioneer and is at the forefront from a technological point of view with the production facility located in Framingham (Massachusetts). As we can see from the graph above there are a total of 8 products of which the CTX130 is in the clinical phase and this represents a well-diversified and broad portfolio.

Concerning the authorization process, again according to management, there could be an accelerated path mainly due to unsatisfied market demand.

‘Our belief is that there is a path to get an accelerated approval of a single-arm trial. Obviously, we have to follow that with randomized controlled trials and everything else, confirmatory trials. But there is a path to get there because of the unmet need.’

Source: Morgan Stanley 20th Annual Global Healthcare Conference

Related to other competitors in the same allogenic space (it seems a crowdy space) it should be underlined that the main metrics for which a program can be approved are durability and lasting remission. At the moment CRSP and Allogene (ALLO) are the companies that have recorded the best results.

CRSP began the collaboration with Vertex in 2015. Vertex is a biotechnology company involved in cystic fibrosis diseases. Based on TDT, and SCD programs the companies decided to sign an agreement for the development and commercialization of the CTX001 product. The agreement provides that Vertex can deal with the marketing of the product both in the US and in Europe and this certainly represents a positive aspect for CRSP as it has the possibility of relying on a much larger company with the expertise to market pharma products in the best possible ways.

ViaCyte is a private biotech company focused on stem cell therapies for type 1 diabetes (T1D). ViaCyte is also controlled by Vertex. CRSP and ViaCyte begin a development and commercialization agreement for diabetes type 1 and 2 products.

According to Statista the market size of CRISPR gene editing worldwide is expected to grow by 33% yearly until 2031.

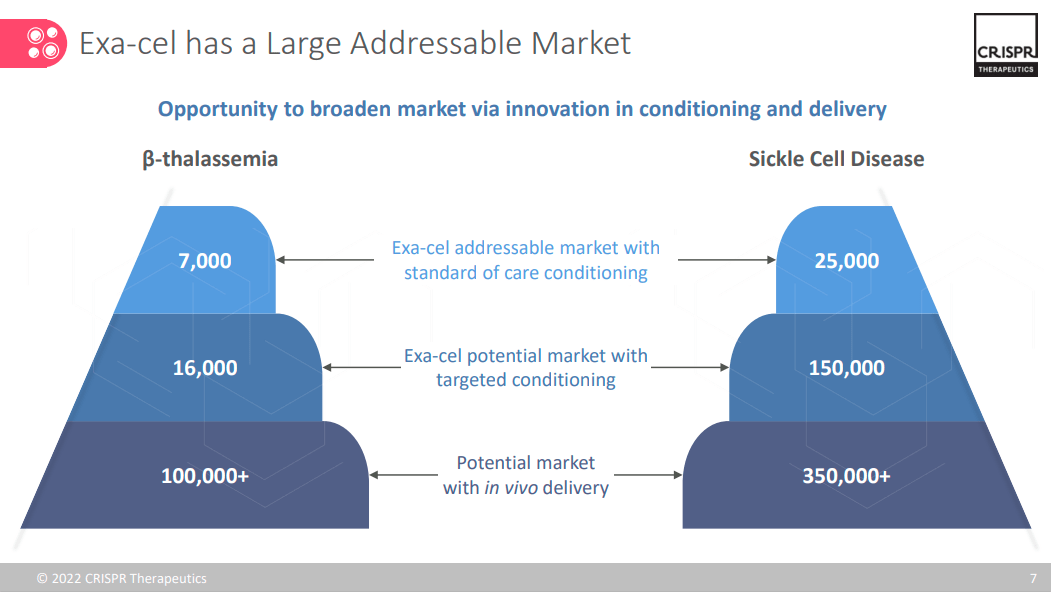

If we look only at the TDY and SCD segments we can instead establish a standard capacity of 32,000 treatable units. This figure grows exponentially if we assume the extension to in-vivo treatments.

CRISPR Corporate Overview Q4 – 22

CRISPR Corporate Overview Q4 – 22

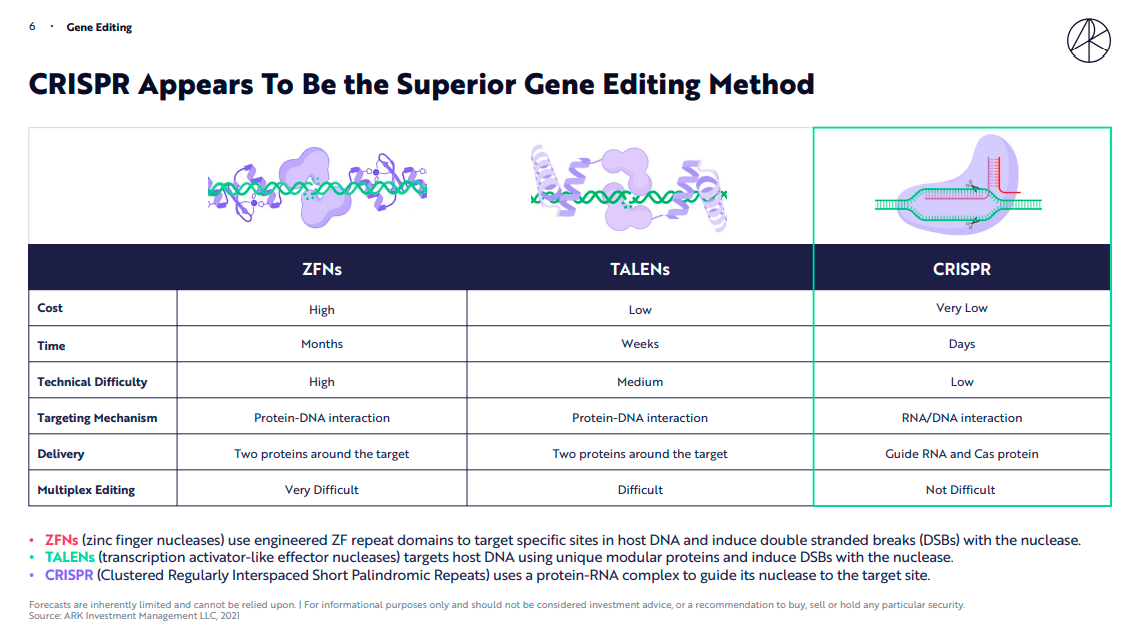

Instead, going into the merits of the comparison between different methodologies in gene editing according to the study by Ark Invest, CRISPR turns out to be the best in terms of cost, implementation time, and technical difficulty.

ARK Invest Genomic Revolution

ARK Invest Genomic Revolution

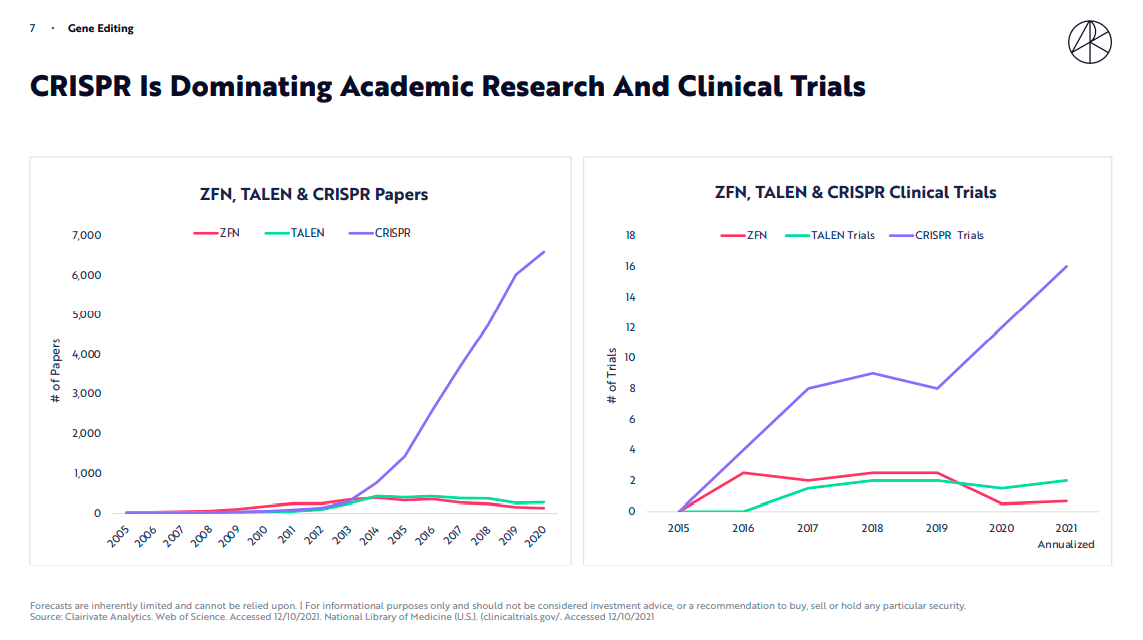

Also from the point of view of publications and above all clinical trials, we can underline how CRISPR represents the most studied and widespread method.

ARK Invest Genomic Revolution

ARK Invest Genomic Revolution

Based on the above, we could deduce that the CRISPR technology market is estimated to grow very strongly in the coming years and that the methodology could represent the best solution for related disease treatment.

It is almost impossible to carry out a CRSP quantitative evaluation as the assumptions on Revenue, EPS, Cash Flow, Growth rate and other income parameters would be very risky and, in all likelihood, very untrue at this stage.

So I decided to use only ‘certain’ parameters available and evaluate the data concerning the sector average or direct competitors. It is therefore a relative and qualitative assessment.

Using the Price to Book Value parameter we can have a relative view of how the Company performs related to the Sector.

Seeking Alpha

Seeking Alpha

CRSP P/B (TTM) is 1.63 and it is quite a high value but if compared to the Sector Median of 1.97 we can state that CRSP performs better than 17.35%. Even if we move on to the P/B (FWD) the figure passes to 1.76 and if compared with the Sector Median, CRSP continues to perform even better than 30.3%.

From the balance sheet point of view, comparing the data with the reference sector, the share price seems to have a good evaluation.

Moving on to a more detailed comparison, I have selected the main CRISPR start-ups that have obtained the most starting funds:

Beam Therapeutics Inc. (BEAM)

Editas Medicine, Inc. (EDIT)

Intellia Therapeutics, Inc. (NTLA)

Verve Therapeutics, Inc. (VERV)

Using P/B value comparison:

CRSP

BEAM

EDIT

NTLA

VERV

Price/Book Vale (TTM)

1.63

3.77

1.44

3.24

2.13

We can see how CRSP is the second-best choice. Only EDIT has a better ratio.

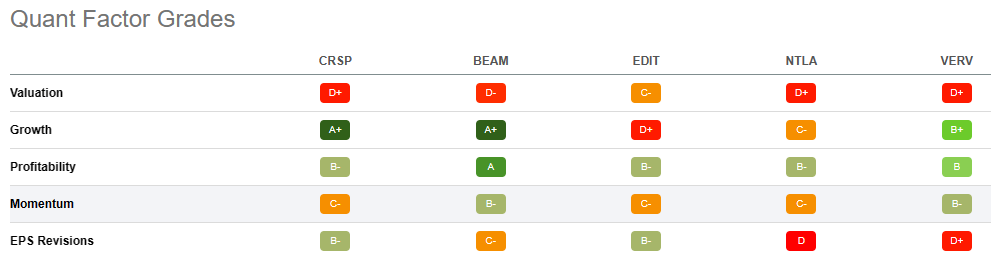

Using Seeking Alpha’s Quant Ratings we have a ‘Buy’ verdict related to the ‘Hold’ rating of the others company.

Seeking Alpha

Seeking Alpha

Under the Quant Factor Grades point of view, we can see how CRSP is outstanding in Growth with an ‘A+’ rate but in Valuation EDIT is preferable.

This comparison allows us to understand how at this moment CRSP could be the best choice with global factor grades in his favor.

Seeking Alpha

Seeking Alpha

The risks are many, high, and difficult to quantify. Uncertainties and high volatility may characterize the business trend (and the share price) in the coming years.

Although the market and the technology used seem to enjoy extremely favorable winds, the sale of products is entrusted to approvals by the Regulatory (FDA and EMA) and this represents a high risk in terms of costs and market timing. To date, no one can guarantee when it will be possible to commercialize the CTX001(the first company product). And this fact represents a high risk also for future products.

Even the product’s selling price may not be definable by the CRSP itself but is subject to exogenous factors that are difficult to predict and which could represent a concrete risk of economic sustainability.

Collaboration with Vertex represents a great advantage in the product’s marketing on the one hand but on the other hand, it could also represent an operational constraint if the interests of the two companies were no longer aligned.

CRISPR identifies a disruptive technology that looks set to enjoy massive growth in the years to come. CRSP possesses the know-how to face this very demanding challenge but which could be a harbinger of great satisfaction in the long term. The company balance sheet data, at the moment, are strong and allow you to continue to innovate. In terms of relative valuation, the company seems to be the best in the sector and therefore represents a good investment opportunity for those who want to bet on gene-editing CRISPR methodology. My rating is Buy.

This article was written by

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.